Mortgage refinancing can be one of the smartest financial moves homeowners make—or one of the most expensive mistakes if done incorrectly.

With mortgage rates constantly changing, millions of homeowners are asking:

- Should I refinance my mortgage in 2026?

- Is refinancing worth the closing costs?

- How much can refinancing save me monthly?

- Does a cash-out refinance make sense?

- When is the best time to refinance?

The answer depends on your financial goals, credit profile, home equity position, loan structure, and long-term housing plans.

For some homeowners, refinancing may reduce monthly payments by hundreds of dollars. Others may use refinancing to eliminate high-interest debt, shorten loan terms, or access home equity for renovations, investment properties, or business opportunities.

However, refinancing also carries risks.

Closing costs, extended loan terms, interest expenses, and credit impacts can outweigh the benefits if refinancing is not planned strategically.

This complete beginner-friendly guide explains everything homeowners need to know about refinancing in 2026, including:

- When refinancing makes financial sense

- Mortgage refinance break-even calculator examples

- Cash-out refinance pros and cons

- Fixed-rate vs adjustable-rate refinancing

- Mortgage lender comparison strategies

- Current mortgage rate trends

- Step-by-step refinance application process

- Common refinancing mistakes to avoid

By the end of this article, you will understand exactly how mortgage refinancing works and whether refinancing aligns with your financial goals.

What Is Mortgage Refinancing?

Mortgage refinancing replaces your current home loan with a new mortgage.

The new loan typically includes updated terms such as:

- Lower interest rate

- Different loan duration

- Reduced monthly payment

- Adjustable or fixed rates

- Cash-out borrowing options

Homeowners refinance for several reasons:

- Lower monthly expenses

- Reduce interest costs

- Access home equity

- Consolidate debt

- Pay off mortgage faster

- Switch from ARM to fixed-rate loan

The refinancing lender pays off the original mortgage, and the homeowner begins making payments under the new loan agreement.

When Refinancing Makes Sense

Refinancing is not automatically beneficial.

It usually makes the most sense under certain financial conditions.

1. Interest Rates Have Dropped

One of the most common reasons homeowners refinance is to secure a lower mortgage rate.

Even a 1% reduction in interest may save tens of thousands of dollars over the life of a loan.

Example:

- Current mortgage: 7.5%

- Refinance rate: 6.2%

- Remaining balance: $400,000

Potential savings could exceed several hundred dollars monthly.

2. You Want Lower Monthly Payments

Refinancing into a longer loan term may reduce monthly obligations.

This strategy may help homeowners:

- Improve cash flow

- Reduce financial stress

- Lower debt-to-income ratios

- Create emergency savings flexibility

However, longer terms may increase total lifetime interest costs.

3. You Want to Pay Off Your Mortgage Faster

Some homeowners refinance from a 30-year mortgage into a 15-year loan.

Benefits may include:

- Faster equity growth

- Lower lifetime interest payments

- Quicker debt elimination

This strategy works best for financially stable households capable of handling higher monthly payments.

4. You Need Cash From Home Equity

A cash-out refinance allows homeowners to borrow against accumulated home equity.

This strategy is often used for:

- Home renovations

- Debt consolidation

- Medical expenses

- Business funding

- Investment opportunities

Cash-out refinance pros and cons should always be evaluated carefully because the home becomes collateral for borrowed funds.

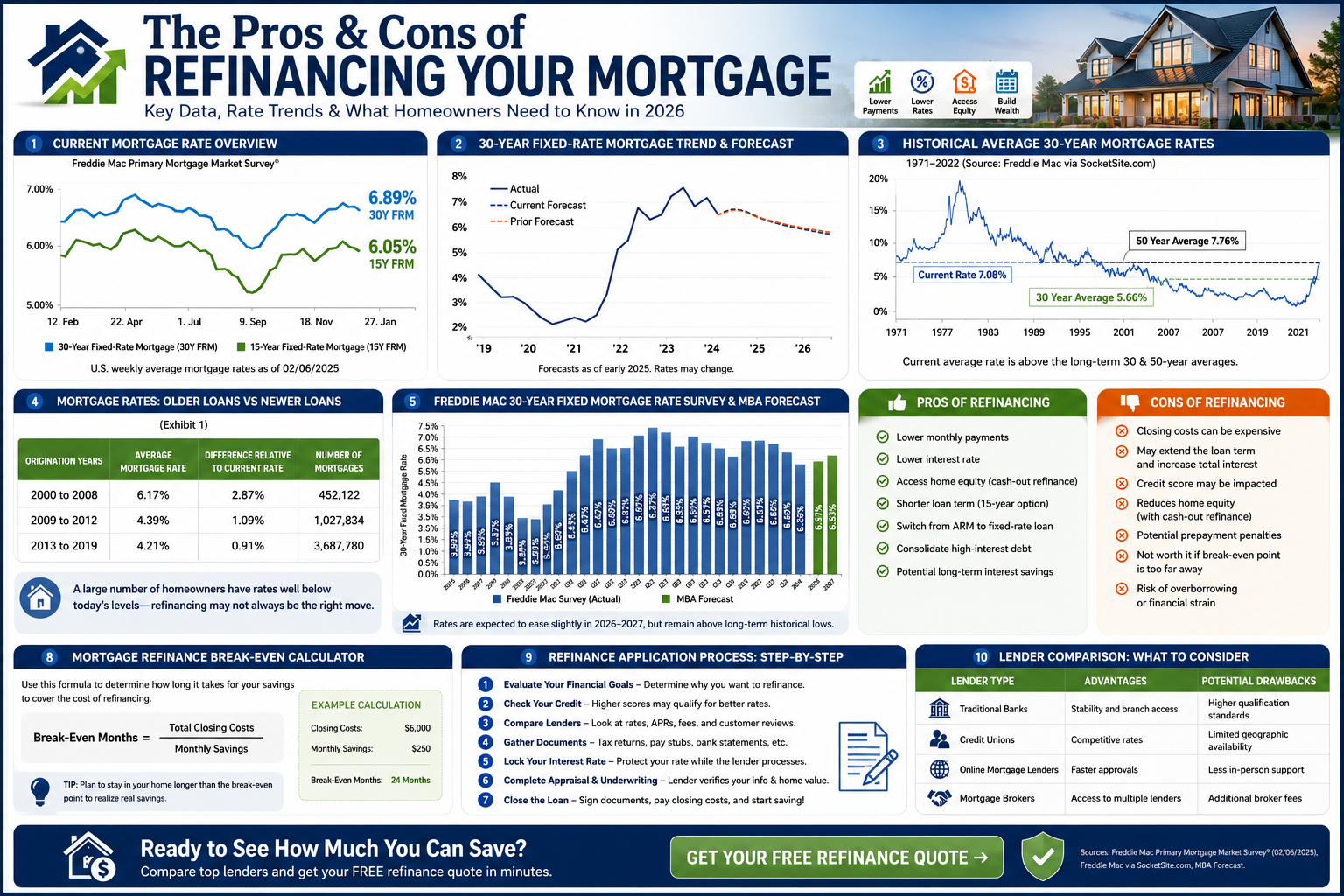

Understanding Mortgage Refinance Break-Even Points

Before refinancing, homeowners should calculate the break-even point.

The break-even point determines how long it takes monthly savings to exceed refinance costs.

Mortgage Refinance Break-Even Calculator Formula

\text{Break-Even Months} = \frac{\text{Total Closing Costs}}{\text{Monthly Savings}}

Example Break-Even Calculation

Suppose:

- Closing costs = $6,000

- Monthly savings = $250

Break-even calculation:

- $6,000 ÷ $250 = 24 months

This means the homeowner must remain in the home for at least 24 months before refinancing produces net financial savings.

Why the Break-Even Calculator Matters

The mortgage refinance break-even calculator is one of the most important tools homeowners can use.

It helps determine whether refinancing truly creates long-term financial value.

If a homeowner plans to move before reaching the break-even point, refinancing may not make financial sense.

Pros of Refinancing Your Mortgage

Mortgage refinancing offers several potential financial advantages.

1. Lower Monthly Mortgage Payments

Reducing monthly expenses is often the primary motivation for refinancing.

Benefits may include:

- Improved cash flow

- Increased savings capacity

- Easier budgeting

- Reduced financial stress

This is particularly important during periods of inflation or economic uncertainty.

2. Lower Interest Rates

A lower mortgage rate can dramatically reduce total borrowing costs.

Even small reductions may create substantial long-term savings.

Homeowners with improved credit scores often qualify for better rates than when they originally purchased their homes.

3. Shorter Loan Terms

Refinancing into a shorter mortgage term may help homeowners:

- Build equity faster

- Reduce lifetime interest

- Become debt-free sooner

Many financially disciplined households prefer 15-year mortgages for this reason.

4. Accessing Home Equity

Cash-out refinancing allows homeowners to unlock equity without selling their property.

This can be useful for:

- Renovation projects

- Investment opportunities

- Education expenses

- High-interest debt consolidation

However, homeowners must manage borrowed funds responsibly.

5. Switching Loan Types

Some homeowners refinance to move from:

- Adjustable-rate mortgages (ARMs)

- Interest-only loans

- Balloon mortgages

into stable fixed-rate loans.

This can improve payment predictability and reduce future rate uncertainty.

Cons of Refinancing Your Mortgage

Despite the benefits, refinancing also carries important drawbacks.

1. Closing Costs Can Be Expensive

Refinancing often includes:

- Origination fees

- Appraisal fees

- Title insurance

- Underwriting costs

- Attorney fees

- Recording fees

Closing costs typically range from 2%–6% of the loan amount.

For larger mortgages, costs can become substantial.

2. Extending the Loan Term

Refinancing into another 30-year mortgage resets the amortization schedule.

This may increase total interest paid over time—even if monthly payments decrease.

Many homeowners focus only on monthly savings while ignoring long-term borrowing costs.

3. Credit Score Impact

Mortgage refinancing involves:

- Hard credit inquiries

- New debt accounts

- Underwriting reviews

This may temporarily affect credit scores.

Most impacts are relatively minor for borrowers with strong financial profiles.

4. Reduced Home Equity

Cash-out refinancing reduces home equity because homeowners borrow against their property value.

This may increase financial risk during housing market downturns.

5. Potential Prepayment Penalties

Some mortgages include prepayment penalties for early loan payoff.

Borrowers should review existing loan terms carefully before refinancing.

30-Year vs 15-Year vs ARM Refinance Comparison

| Loan Type | Average Rate | Monthly Payment | Best For | Main Risk |

|---|---|---|---|---|

| 30-Year Fixed | Moderate | Lower | Budget stability | Higher lifetime interest |

| 15-Year Fixed | Lower | Higher | Faster payoff | Larger monthly payments |

| Adjustable-Rate Mortgage (ARM) | Initially lower | Lower initially | Short-term ownership | Future rate increases |

Current Mortgage Rate Trends in 2026

Mortgage rates continue fluctuating due to:

- Federal Reserve policy

- Inflation

- Bond market activity

- Housing supply

- Economic growth

Freddie Mac’s weekly mortgage survey remains one of the most widely referenced mortgage rate indicators in the industry.

Historically:

- Falling inflation often pressures rates downward

- Strong labor markets may keep rates elevated

- Federal Reserve decisions heavily influence mortgage pricing

Homeowners considering refinancing should monitor rate trends regularly.

How Much Equity Do You Need to Refinance?

Most lenders prefer homeowners to maintain at least:

- 15%–20% equity

for conventional refinancing approval.

Cash-out refinancing often requires:

- Strong credit

- Stable income

- Lower debt-to-income ratios

Government-backed refinance programs may offer different requirements.

Mortgage Refinance Application Process

Refinancing typically follows several steps.

Step 1: Evaluate Financial Goals

Homeowners should first identify why they want to refinance.

Questions include:

- Lower payment?

- Faster payoff?

- Debt consolidation?

- Cash access?

- Rate stability?

Clear objectives improve decision-making.

Step 2: Check Credit Scores

Mortgage lenders heavily evaluate creditworthiness.

Higher credit scores often qualify for:

- Lower rates

- Better terms

- Reduced fees

Improving credit before applying may produce substantial savings.

Step 3: Compare Mortgage Lenders

Not all lenders offer identical pricing.

Homeowners should compare:

- Interest rates

- APRs

- Closing costs

- Customer reviews

- Loan products

- Service quality

Shopping multiple lenders may save thousands.

Mortgage Lender Comparison Table

| Lender Type | Advantages | Potential Drawbacks |

|---|---|---|

| Traditional Banks | Stability and branch access | Higher qualification standards |

| Credit Unions | Competitive rates | Limited geographic availability |

| Online Mortgage Lenders | Faster approvals | Less in-person support |

| Mortgage Brokers | Access to multiple lenders | Additional broker fees |

Step 4: Gather Financial Documents

Most refinance applications require:

- Tax returns

- W-2s or 1099s

- Bank statements

- Pay stubs

- Mortgage statements

- Homeowners insurance documents

Organized documentation accelerates underwriting.

Step 5: Lock Your Interest Rate

Rate locks protect borrowers from market increases during loan processing.

Lock periods commonly range from:

- 15 days

- 30 days

- 60 days

Longer locks may cost more.

Step 6: Complete Appraisal and Underwriting

Lenders evaluate:

- Property value

- Income stability

- Employment

- Debt obligations

- Credit history

Underwriters determine final approval conditions.

Step 7: Close the Loan

At closing:

- Old mortgage gets paid off

- New loan activates

- Borrowers sign updated documents

Federal law generally provides a three-day rescission period for many refinance transactions.

Cash-Out Refinance Pros and Cons

Cash-out refinancing deserves special consideration because it increases debt exposure.

Cash-Out Refinance Pros

Benefits may include:

- Lower interest rates than personal loans

- Access to large amounts of capital

- Potential debt consolidation savings

- Home improvement financing

Cash-Out Refinance Cons

Risks include:

- Reduced home equity

- Increased foreclosure risk

- Larger loan balances

- Higher total interest costs

Homeowners should avoid using home equity irresponsibly for unnecessary consumer spending.

Common Mortgage Refinancing Mistakes

Many homeowners refinance without fully evaluating long-term consequences.

Focusing Only on Monthly Payments

Lower payments do not always equal better financial outcomes.

Total lifetime borrowing costs matter.

Ignoring Closing Costs

Some borrowers underestimate refinance expenses significantly.

Always calculate total costs carefully.

Failing to Shop Multiple Lenders

Mortgage pricing varies substantially between lenders.

Obtaining multiple quotes is critical.

Refinancing Too Frequently

Repeated refinancing may increase costs and extend debt unnecessarily.

Choosing the Wrong Loan Type

Adjustable-rate mortgages may become risky during rising interest rate environments.

Refinancing for Debt Consolidation: Is It Worth It?

Some homeowners use refinancing to consolidate:

- Credit card debt

- Personal loans

- Medical bills

- Auto loans

This strategy may reduce interest costs substantially.

However, unsecured debt becomes secured by the home.

Failure to repay could jeopardize home ownership.

Should Retirees Refinance?

Retirees sometimes refinance to:

- Reduce fixed monthly expenses

- Improve retirement cash flow

- Eliminate adjustable-rate exposure

However, lenders still evaluate:

- Income

- Assets

- Creditworthiness

- Debt obligations

Retirees should assess whether refinancing aligns with long-term retirement goals.

Is 2026 a Good Time to Refinance?

The answer depends on:

- Current mortgage rate

- Credit profile

- Equity position

- Financial goals

- Time remaining in the home

For some homeowners, refinancing in 2026 may create substantial long-term savings.

Others may benefit more from maintaining existing mortgage structures.

Personal financial analysis is essential.

Should You Refinance Your Mortgage in 2026?

Mortgage refinancing can be an incredibly powerful financial tool when used strategically.

For many homeowners, refinancing may:

- Lower monthly expenses

- Reduce interest costs

- Improve cash flow

- Access home equity

- Accelerate debt repayment

However, refinancing also involves:

- Closing costs

- Loan restructuring

- Credit considerations

- Long-term financial tradeoffs

The smartest homeowners evaluate refinancing based on total financial impact—not just short-term payment reductions.

Using a mortgage refinance break-even calculator, comparing lenders carefully, and reviewing long-term goals can help homeowners make informed refinancing decisions.

Get Your Free Refinance Quote

If you are considering refinancing, now is the time to compare rates, review loan options, and evaluate your potential savings.

Before choosing a lender:

- Compare APRs

- Review closing costs

- Analyze break-even timelines

- Evaluate fixed vs ARM options

- Understand cash-out refinance risks

A free refinance quote may help you determine whether refinancing aligns with your financial goals and long-term homeownership strategy.

Frequently Asked Questions About Mortgage Refinancing

What does it mean to refinance a mortgage?

Mortgage refinancing means replacing your existing home loan with a new mortgage that typically offers different terms, interest rates, or repayment structures. Homeowners refinance to lower payments, reduce interest costs, access home equity, or change loan terms.

Should I refinance my mortgage in 2026?

Whether refinancing makes sense in 2026 depends on your current mortgage rate, credit score, home equity, financial goals, and how long you plan to stay in your home. Refinancing may be beneficial if you can significantly lower your interest rate or improve your loan structure.

How much does mortgage refinancing cost?

Refinancing usually includes closing costs ranging from 2% to 6% of the loan amount. These costs may include appraisal fees, lender fees, title insurance, underwriting charges, attorney fees, and recording fees.

What is a mortgage refinance break-even point?

The break-even point is the amount of time it takes for your monthly refinance savings to exceed the total refinancing costs. Homeowners often use a mortgage refinance break-even calculator to determine whether refinancing is financially worthwhile.

How do you calculate mortgage refinance break-even?

You can calculate the break-even point using this formula:

Break-Even Months = Total Closing Costs ÷ Monthly Savings

For example, if refinancing costs $5,000 and saves $250 monthly, the break-even point would be 20 months.

What are the benefits of refinancing a mortgage?

Mortgage refinancing may provide several benefits including lower monthly payments, reduced interest rates, shorter loan terms, faster equity growth, debt consolidation opportunities, and access to home equity through cash-out refinancing.

What are the disadvantages of refinancing?

Potential drawbacks include closing costs, extended loan terms, temporary credit score impacts, reduced home equity, and the possibility of paying more interest over time if the loan term resets.

What is a cash-out refinance?

A cash-out refinance allows homeowners to replace their mortgage with a larger loan and receive the difference in cash. Many homeowners use cash-out refinancing for renovations, debt consolidation, investments, or major expenses.

Is cash-out refinancing risky?

Yes. Cash-out refinancing increases your loan balance and reduces home equity. Since your home serves as collateral, failure to repay the loan could increase foreclosure risk.

How much equity do I need to refinance?

Most lenders prefer homeowners to maintain at least 15% to 20% equity for conventional refinancing approval. Cash-out refinancing may require additional equity depending on the lender and loan program.

Does refinancing hurt your credit score?

Refinancing may temporarily affect your credit score due to hard credit inquiries and the creation of a new loan account. However, impacts are usually minor for borrowers with strong credit histories.

Can refinancing lower my monthly mortgage payment?

Yes. Refinancing into a lower interest rate or longer loan term may reduce your monthly mortgage payment significantly, improving household cash flow and budgeting flexibility.

Is it better to refinance into a 15-year mortgage?

A 15-year mortgage may help homeowners pay off debt faster and reduce lifetime interest costs. However, monthly payments are typically higher than 30-year mortgage payments.

What is the difference between fixed-rate and adjustable-rate mortgages?

Fixed-rate mortgages maintain the same interest rate throughout the loan term, while adjustable-rate mortgages (ARMs) may change periodically based on market conditions. Fixed-rate loans provide payment stability, while ARMs may offer lower initial rates but carry future rate risks.

How long does the refinance process take?

The mortgage refinance process usually takes between 30 and 45 days depending on lender processing times, appraisal scheduling, underwriting reviews, and document verification.

What documents are required for mortgage refinancing?

Lenders commonly require tax returns, W-2s or 1099s, pay stubs, bank statements, mortgage statements, identification documents, and homeowners insurance information.

Can retirees refinance their mortgage?

Yes. Retirees may refinance if they meet lender qualification requirements involving income, assets, credit scores, and debt-to-income ratios. Many retirees refinance to lower fixed monthly expenses.

Can refinancing help consolidate debt?

Yes. Some homeowners use refinancing to consolidate high-interest debts such as credit cards and personal loans into lower-interest mortgage debt. However, unsecured debt becomes secured by the home.

How often can you refinance your mortgage?

There is no strict legal limit on refinancing frequency, but lenders may impose waiting periods depending on the loan type. Frequent refinancing may increase costs and extend repayment timelines unnecessarily.

What is the best time to refinance a mortgage?

The best time to refinance is typically when mortgage rates decline significantly, your credit score improves, your home value increases, or your financial goals change.

Can refinancing remove private mortgage insurance (PMI)?

Yes. If your home equity exceeds lender requirements, refinancing may eliminate private mortgage insurance, reducing monthly housing expenses.

Are online mortgage lenders safe?

Many online mortgage lenders are legitimate and highly competitive. Homeowners should review lender licensing, customer reviews, APR disclosures, fees, and Better Business Bureau ratings before applying.

Do mortgage rates change daily?

Yes. Mortgage rates can fluctuate daily based on inflation, Federal Reserve policy, bond markets, housing demand, and overall economic conditions.

What is Freddie Mac’s mortgage survey?

Freddie Mac’s Primary Mortgage Market Survey is one of the most widely referenced reports tracking average U.S. mortgage rates. Many homeowners and lenders use it to monitor mortgage rate trends.

Should homeowners compare multiple refinance lenders?

Absolutely. Comparing multiple lenders may help homeowners secure lower rates, reduced fees, better loan terms, and improved customer service experiences.